EBA Strengthens ESG Disclosure Framework via Consultation, Data Hub, and Technical Package

The EBA’s recent publications mark a significant step in operationalising ESG risk disclosures through regulatory alignment, digital infrastructure, and technical implementation. These initiatives respond to evolving prudential requirements under CRR3 and reflect the growing emphasis on consistency, proportionality, and accessibility of sustainability-related information in the EU banking sector.

In May 2025, the European Banking Authority (EBA) released a set of key initiatives aimed at strengthening ESG integration in supervisory practices. These included a public consultation on ESG disclosure requirements, an onboarding plan for the Pillar 3 Data Hub, and the finalisation of reporting framework version 4.1. Together, these developments reflect the EBA’s focus on improving the consistency, accessibility, and relevance of disclosures in the EU banking sector.

Consultation Objectives and ESG Disclosure Enhancements

The consultation proposes amendments to the Implementing Technical Standards (ITS) under the Capital Requirements Regulation (CRR) to incorporate new disclosure requirements introduced by CRR3. These cover ESG risks, equity exposures, and exposures to shadow banking entities, and include alignment with the EU Taxonomy Regulation where relevant.

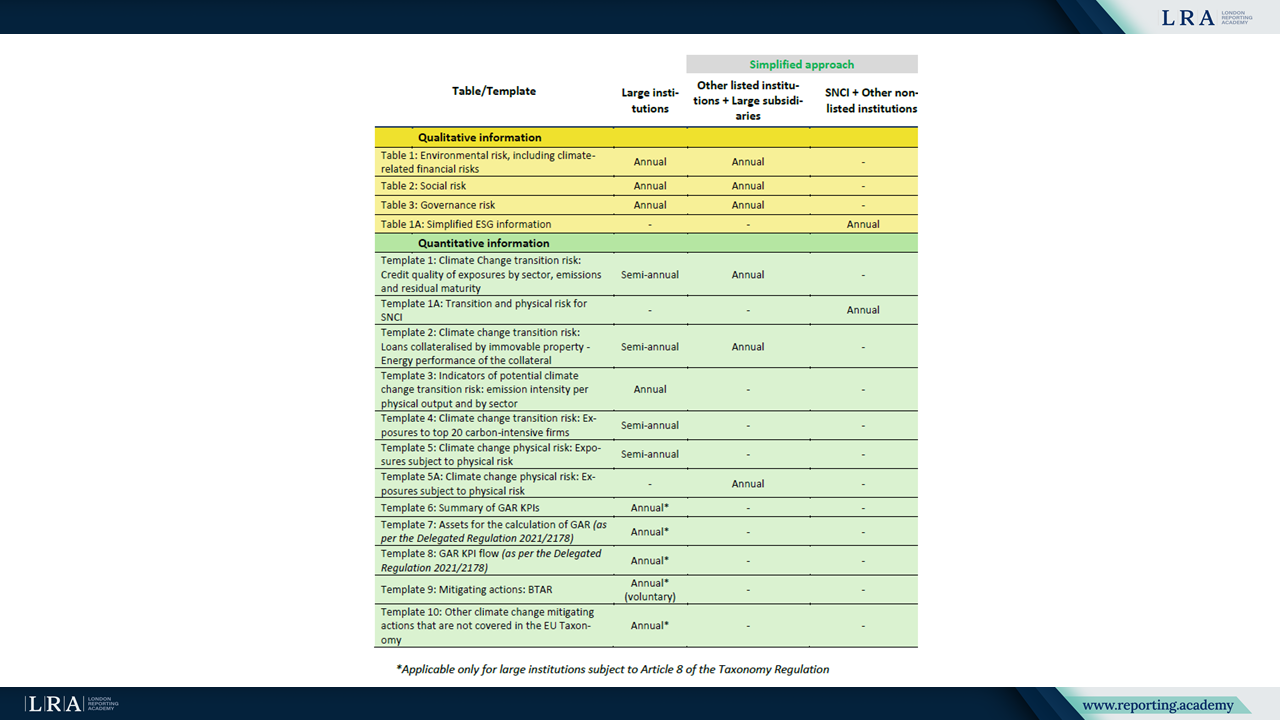

The consultation outlines revisions to ESG disclosure templates to reflect new CRR3 requirements and improve clarity for institutions. The EBA proposes revisions to the Green Asset Ratio (GAR) and introduces the Banking Book Taxonomy Alignment Ratio (BTAR), which extends taxonomy alignment assessments across a wider set of exposures. The revised templates also expand requirements on financed emissions, including Scope 3, and add more detailed sectoral breakdowns using updated NACE codes. These measures are intended to strengthen climate risk analysis and comparability.

In line with the European Commission’s omnibus proposal to streamline sustainability reporting and reduce administrative burden, the EBA has adopted a proportionate approach to ESG disclosures. The proposed framework differentiates disclosure requirements based on an institution’s type, size, and complexity, with simplified reporting for small, non-listed, and less complex entities.

The full sets of templates applicable to different categories of institutions, along with their respective reporting frequencies, are summarised in the table below:

Source: Consultation Paper

The EBA proposes enhanced reporting of exposures to shadow banking entities to support systemic risk monitoring. The EBA proposes updates to equity exposure disclosure templates in line with Article 438(e) of CRR3, reflecting transitional arrangements and ensuring consistent reporting as CRR3 is implemented.

Digital Infrastructure: Pillar 3 Data Hub

To support these disclosures, the EBA is developing the Pillar 3 Data Hub (P3DH), a central platform for collecting and publishing disclosure data. The onboarding plan outlines a phased rollout between June and November 2025, with institutions grouped by size and complexity. Access will be managed via Microsoft Entra ID and the EUCLID platform.

The overall timeline to complete the onboarding process of large and other institutions for the first implementation of the P3DH is presented below:

Source: Pillar 3 Data Hub: Institutions’ Onboarding Plan

During the transition, institutions may continue publishing on their websites, but must also submit structured data to the Data Hub. This aims to reduce fragmentation and ensure consistency across EU markets.

Technical Enablement: Reporting Framework 4.1

The EBA has finalised the technical package for version 4.1 of its reporting framework. It includes updated data point models, validation rules, and XBRL taxonomies to support structured, machine-readable disclosures. This standardisation underpins the functioning of the Data Hub and helps ensure data quality.

Institutional Impact and Next Steps

These initiatives signal a move toward more transparent and data-driven disclosures. Institutions should assess data readiness, strengthen internal ESG frameworks, and prepare for more detailed reporting requirements under CRR3.

The consultation is open until 21 August 2025. Institutions are encouraged to engage early and plan for implementation.

Conclusion

By aligning reporting standards, infrastructure, and guidance, the EBA is laying the groundwork for more transparent ESG risk disclosures. These developments aim to improve market discipline and foster more comparable and credible sustainability information in the EU banking sector.