CARB Publishes Preliminary Entity List for SB 253 and SB 261

CARB has published a preliminary list of entities that may be in scope of SB 253 and SB 261, marking an early step in implementing California’s climate disclosure programme. The list supports development of the fee regulation and draws on California Secretary of State records through March 2022, so duplicates and omissions are possible. CARB has opened a short survey to validate entries and clarified that inclusion or omission does not determine legal responsibility.

Regulatory Background

In a significant move towards enhanced corporate climate transparency, the California Air Resources Board (CARB) has released a preliminary list of entities that may fall under the reporting obligations of SB 253 and SB 261. These statutes, enacted in 2023 and amended in 2024 through SB 219, establish mandatory GHG emissions disclosures and climate-related financial risk reporting requirements for large companies doing business in California. SB 253 applies to entities with more than $1 billion in annual revenue, while SB 261 applies to entities with more than $500 million in annual revenue. The statutes are codified in Health and Safety Code §§ 38532 and 38533, and SB 219 extends certain deadlines and makes administrative modifications. CARB indicates it is at the beginning of a public process to develop regulations and guidance and identifies administrative efficiency and programme exportability as foundational principles. The framework is intended to align with globally recognised standards such as the TCFD and aims to produce accurate, comparable and decision‑useful information for investors and consumers.

The Preliminary List: Structure and Limitations

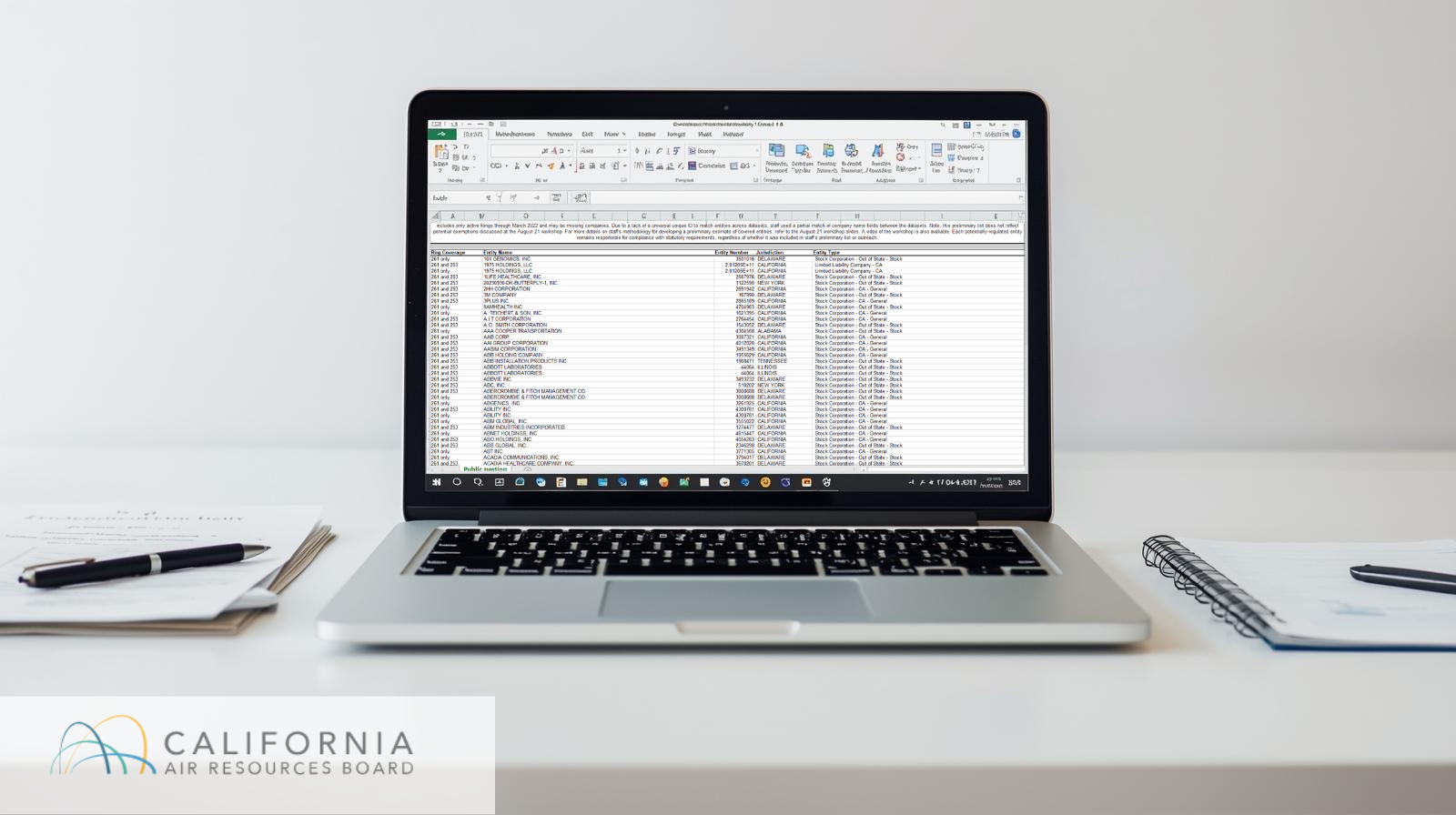

Published on 23 September 2025, the preliminary list includes approximately 4,150 entries. It identifies companies potentially subject to either or both regulatory regimes: SB 253, which mandates public disclosure of Scope 1, 2, and eventually Scope 3 GHG emissions; and SB 261, which requires biennial reporting on climate-related financial risks and mitigation strategies.

CARB developed the list using publicly available data from the California Secretary of State (SoS), relying on active business entity filings through March 2022. Due to the absence of a universal unique identifier across datasets, partial name matching was used, which has led to duplicates and inconsistencies in regulatory classification for some entities. For example, a company like 1975 Holdings, LLC appears more than once, associated alternately with SB 261 only and with both SB 253 and SB 261.

The list does not reflect potential exemptions discussed during CARB’s 21 August 2025 public workshop, and stakeholders are encouraged to provide feedback through an eight‑question voluntary survey. Importantly, CARB has clarified that presence or absence from the list does not determine legal responsibility, as each entity remains independently accountable for assessing and meeting compliance obligations.

Key Deadlines and Framework Alignment

For companies within the scope of SB 253, the first reporting deadline for Scope 1 and Scope 2 emissions is proposed for 30 June 2026, with Scope 3 disclosures required from 2027. SB 261 requires in‑scope entities to publish a climate‑related financial risk report on their website by 1 January 2026 and to post a public link to CARB’s docket, which will be open from 1 December 2025 to 1 July 2026.

Looking Ahead

As CARB continues to refine its regulatory approach, stakeholder engagement remains critical. Companies must not only confirm their inclusion in the regulatory scope but also assess internal reporting readiness and supply chain data quality, particularly in anticipation of Scope 3 requirements. The design of the fee regulation, for which the preliminary list serves as a foundation, will also shape the operational burden for in-scope entities.

Ultimately, California’s dual-disclosure framework reflects a broader regulatory shift towards embedding climate risk and accountability into corporate governance. The months ahead will be pivotal in translating legislative ambition into robust, actionable compliance infrastructure.